One of the biggest areas of focus in medicine right now in the US is how to drive down costs.

With the record breaking inflation, the rising costs are becoming a burden to healthcare providers.

And now, the industry is looking for ways to effectively manage this situation.

That’s where MultiPlan comes in, the company offers customized cost management solutions to struggling healthcare providers.

Whether it be by improving care, monitoring spending patterns, identifying high cost patients to manage more closely sooner, or just identifying fraud, MultiPlan is at the heart of lowering healthcare costs.

The company uses technology-enabled provider network, negotiation, claim pricing and payment accuracy services to manage the cost structure better.

With so much money and innovation flowing to cost management space in healthcare and the company’s success in making money from its solutions, it’s clear that MultiPlan is a key player to pay attention to and bet on.

Yet, credit rating agencies like S&P rate the company like it’s got a 25% chance of going bankrupt.

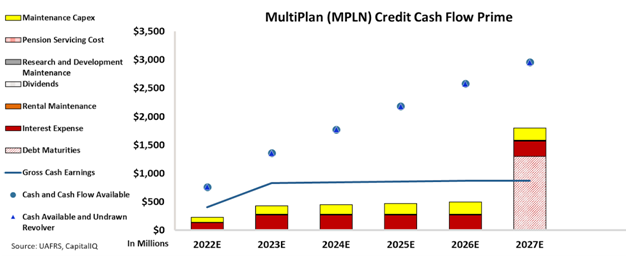

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that MultiPlan’s cash on hand covers all obligations and its cash flows consistently exceed operating obligations for the next six years.

Looking at the CCFP, we can see that the company has no problems meeting its obligations and has no debt burdens that would slow its operations.

Also, considering the company’s positioning in the healthcare industry and its huge profitability by providing these crucial services, it’s not fair to think the company has this big of a chance to go bankrupt.

That is why, MultiPlan gets an IG3- rating from Valens. This corresponds to a default risk much less than 25% which the rating agencies suggested.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and MultiPlan Corporation Tearsheet

As the Uniform Accounting tearsheet for MultiPlan Corporation (MPLN:USA) highlights, the Uniform P/E trades at 10.4x, which is below the global corporate average of 18.9x and its historical P/E of 12.4x.

Low P/Es require low EPS growth to sustain them. In the case of MultiPlan, the company has recently shown a 229% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, MultiPlan’s Wall Street analyst-driven forecast is for a -7% and -0% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify MultiPlan’s $3 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 is 97x the long-run corporate average. However, cash flows and cash on hand are more than 3x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low credit risk.

Lastly, MultiPlan’s Uniform earnings growth is below its peer averages and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of MultiPlan Corporation (MPLN) credit outlook is the same type of analysis that powers our macro research detailed in the member-exclusive FA Alpha Pulse.