Over the past 12 months, Americans have poured billions of dollars into buying used cars thanks to tight supply and surging demand.

Thanks to critical shortages in semiconductors around the world, today’s smarter cars with onboard computers were stuck on the factory floor. Meanwhile, as folks moved en masse from the city to the suburbs following increased flexibility with work, they needed cars to travel compared to public transportation.

This meant the supply of new cars wasn’t enough to meet demand. Owners of used cars and used car dealerships had some of their best years on record from buyers turning to well-trodden transportation options.

However, another business has benefited from the surge in used cars as well. LKQ Corporation is an aftermarket car part company that specializes in tuning up or keeping older cars on the road.

Before certified pre-owned cars are sold, they are checked over and retrofitted with any new parts needed. Furthermore, older cars require exponentially more parts every year to keep them on the road.

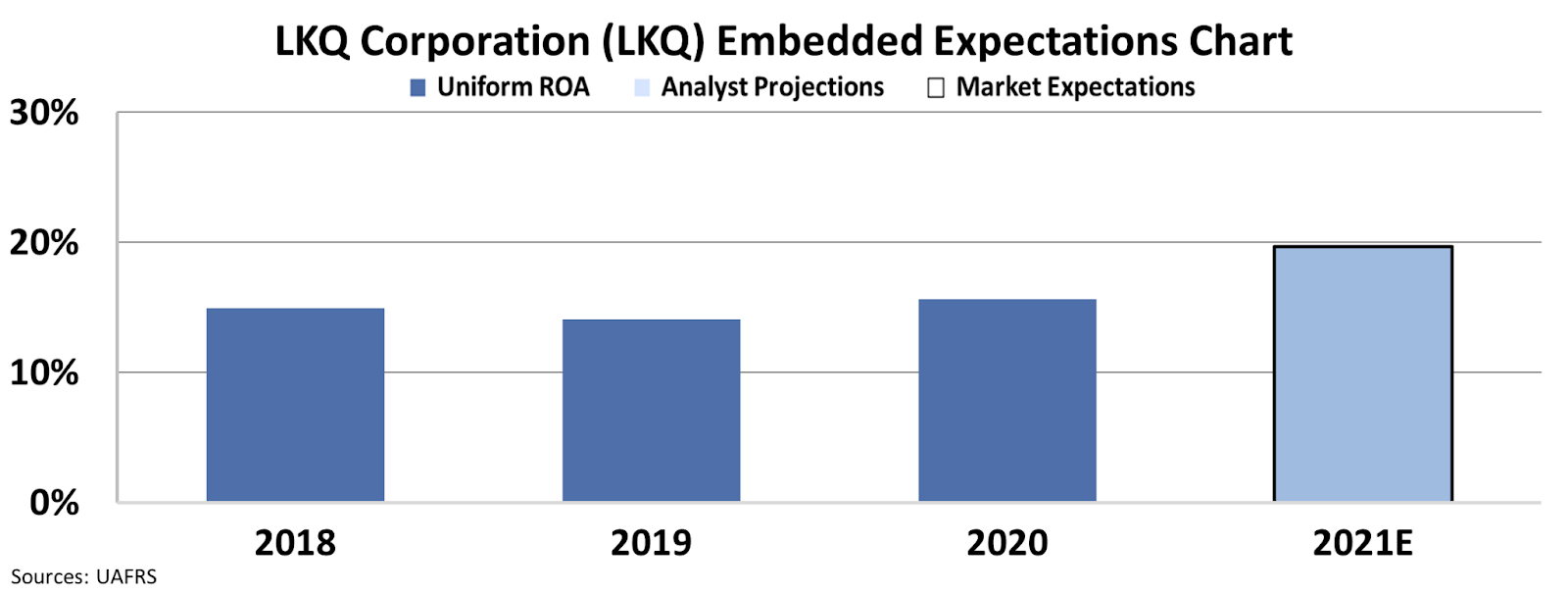

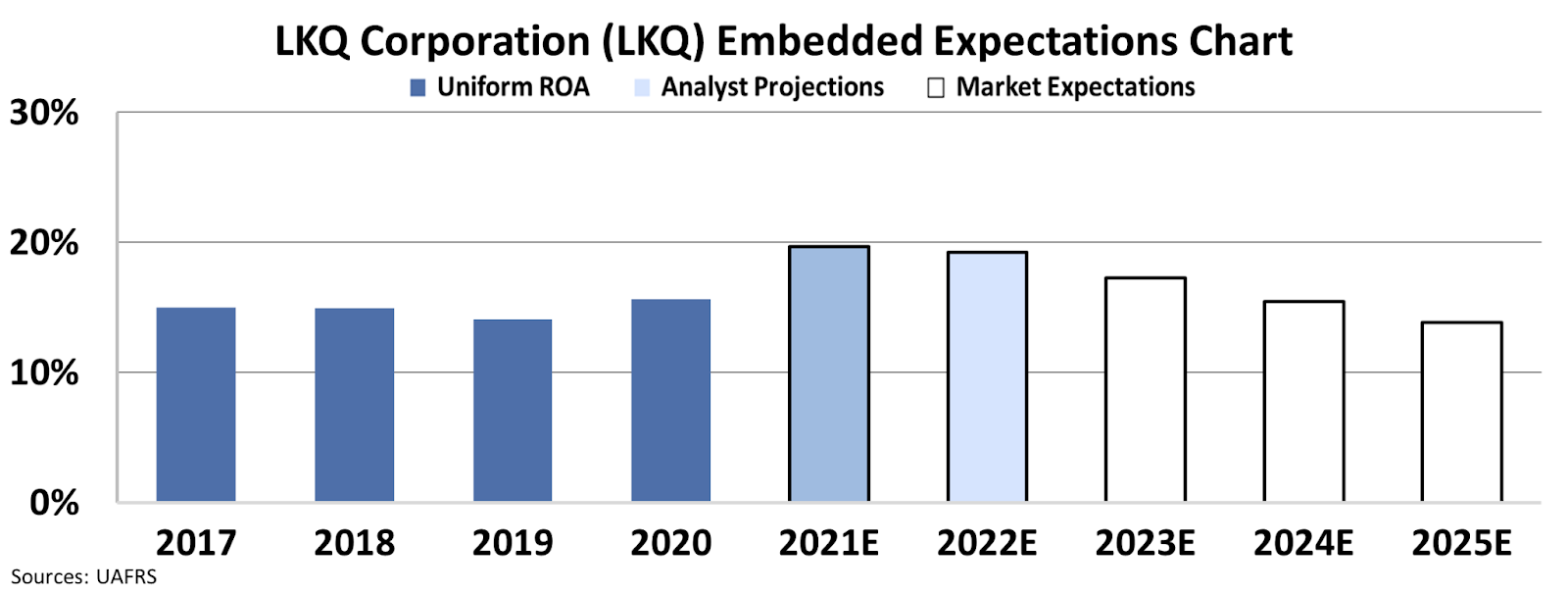

LKQ Corporation has seen Uniform returns spike this year, as more drivers than ever turned to the aftermarket parts company to keep their used cars going. This sent returns climbing from 16% in 2020 to 20% in 2021.

Now, to understand what the market is pricing into the future of the stock, we can turn to our Embedded Expectations analysis.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

However, this type of analysis requires “perfect knowledge” of future inputs, making it harder to get an accurate output. Therefore, turn the model on its by plugging in the current stock price to determine what returns and asset growth the market expects.

As you can see below, the market only believes this boon is temporary, with expectations for returns to slide to new lows of 13%. As used cars will continue to be on the road for years to come, this seems a hasty assumption.

These types of valuations can only be made using Uniform Accounting, which adjusts for over 120 different distortions in GAAP and allows for apples to apples comparisons between companies.

Every day, we are screening for names like LKQ Corporation that have the highest potential to surprise the market and deliver upside for investors.

In our Conviction Long List, we highlight a plethora of names that are currently being overlooked by the market. If you are interested in reading more, you can click here to subscribe.

SUMMARY and LKQ Corporation Tearsheet

As the Uniform Accounting tearsheet for LKQ Corporation (LKQ:USA) highlights, the Uniform P/E trades at 17.0x, which is below the global corporate average of 24.0x, but above its historical P/E of 15.3x.

Low P/Es require low EPS growth to sustain them. In the case of LKQ Corporation, the company has recently shown an 8% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, LKQ Corporation’s Wall Street analyst-driven forecast is a 47% and 2% growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify LKQ Corporation’s $57 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 1% annually over the next three years. What Wall Street analysts expect for LKQ Corporation’s earnings growth is above what the current stock market valuation requires in both 2021 and 2022.

Furthermore, the company’s earning power is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, LKQ Corporation’s Uniform earnings growth is in line with its peer averages and the company is also trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.