Credit rating agencies are still scarred from the energy market crash in 2015, which was a total disaster for both investors and operators alike.

After huge amounts of investment into U.S. shale through 2013 and 2014, when OPEC opened the pumps back up, these cost-sensitive domestic operators were left out to dry.

Thanks to still being scarred from seven years ago, the ratings industry is ignoring the industry’s strong booming demand right now and potential long-lasting tailwinds.

That’s why rating agencies gave a B-rating to Ranger Oil. This translates to a 25% default risk for the company.

Ranger Oil is established in 1882 and the company has 140 years of successful operating history.

As a small-cap name that engages in the exploration and production (E&P) of oil and gas, Ranger is poised to benefit from the current crude oil prices to continue digging.

And along with other big names in E&P, the company is investing to boost its profitability for the long term.

We can figure out if there is a real risk for this high-potential company by examining it through the Credit Cash Flow Prime perspective.

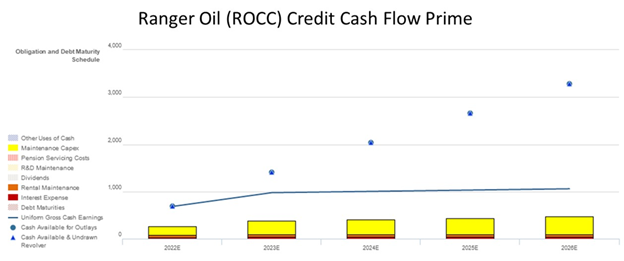

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The B rating suggests a high risk of default, but the CCFP shows that Ranger’s cash flows are more than enough to cover all of its obligations over the next five years, let alone its growing cash base.

The Uniform CCFP shows that the company has zero debt maturity risk and plenty of buffers even if the company was looking to take on debt to fund further growth.

Considering the recent jump in crude oil prices and the effects of the Russian-Ukrainian crisis on demand, Ranger is strategically positioned to benefit from the tailwinds in the sector.

That is why it deserves to be among the investment-grade with an IG3+ rating, which corresponds to a default risk of less than 2%.

Rating agencies seem to miss the potential of successful companies again, by rating Ranger much riskier than the company actually is.

On the other hand, Valens Credit Rating reflects the full story of the company with much less risk than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Ranger Oil Corporation Tearsheet

As the Uniform Accounting tearsheet for Ranger Oil Corporation (ROCC:USA) highlights, the Uniform P/E trades at 3.8x, which is below the global corporate average of 19.7x and its historical P/E of 8.4x.

Low P/Es require low EPS growth to sustain them. In the case of Ranger Oil, the company has recently shown a 141% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ranger Oil’s Wall Street analyst-driven forecast is for a 1,995% decline in EPS and a 48% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ranger Oil’s $32 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 8% annually over the next three years. What Wall Street analysts expect for ZoomInfo’s earnings growth is below what the current stock market valuation requires in 2022 but above that requirement in 2023.

Furthermore, the company’s earning power in 2021 is below the long-run corporate average. Yet, cash flows and cash on hand are 2x its total obligations—including debt maturities and capex maintenance. However, the company has an intrinsic credit risk that is 440bps above the risk-free rate.

Overall, this signals a moderate credit and dividend risk.

Lastly, Ranger Oil’s Uniform earnings growth is well below its peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Ranger Oil Corporation (ROCC) credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.