Due to supply-chain deficiencies, the market cannot quickly cover the rapid surge in consumer demand, causing sky-high inflation. Today’s FA Alpha Daily will examine the Federal Reserve’s strategy to reduce high inflation levels through interest rates.

FA Alpha Daily:

Monday Macro

Powered by Valens Research

The Federal Reserve is trying to control inflation. And historically speaking, the best tool in its arsenal is interest rates.

The Fed controls the rate commercial banks pay to borrow money overnight – called the federal-funds rate. This is effectively the lowest interest rate in the economy.

Raising the federal-funds rate slows borrowing down because banks must increase their own rates to pay for borrowing money. That means loans across the economy become more expensive.

We’ve explained before that we think the U.S. is in the early stages of a supply-chain supercycle. Investment in the supply chain will eventually improve the inflation picture. But it will take time for these changes to take shape.

In the meantime, the Fed is hoping that curtailing demand through higher rates will be a quick inflation fix. But while this solution might make us feel better in the long run, it likely won’t be painless…

Declining demand will lead to slower revenue growth for companies. Additionally, production input costs will lag behind consumer demand movements. So input costs will continue to climb faster than revenue growth, hurting earnings.

Both Morgan Stanley (MS) and Goldman Sachs (GS) project corporate profit margins will decline in the second half of 2022 as a result of the Fed’s actions.

We may even be on the verge of an “earnings recession” on an as-reported basis. In simple terms, that’s two or more consecutive quarters of declining earnings.

Uniform Accounting backs up this theory…

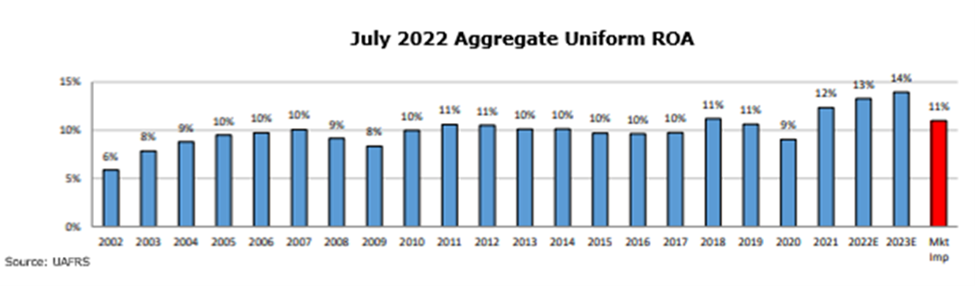

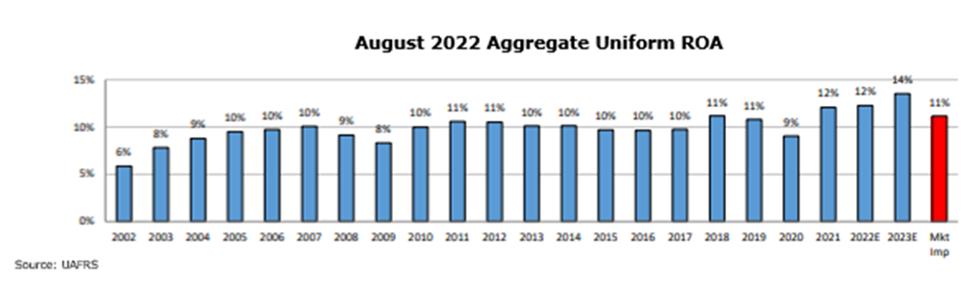

Our aggregate return on assets (“ROA”) data agrees with what Morgan Stanley and Goldman Sachs have been saying. In recent analyses for our paid clients, we’ve warned that an earnings recession is on the horizon.

If we look at what forecasted ROA was in July, we can see that it was projected to rise in 2022.

But when we look at the aggregate ROA chart today, we can see that it is expected to remain flat in 2022.

If ROA remains flat and we don’t see growth in investments by companies, we could really end up seeing an “earnings recession.”

But that doesn’t necessarily spell doom and gloom for the economy.

In fact, things have been playing out just as the Fed hoped. Credit markets are tightening and earnings growth is slowing down.

Plus, expectations for 2023 ROA remain at an all-time high of 14%. So, while high rates might stunt near-term earnings and economic growth, things should start to heal in 2023. Interest-rate hikes will help stabilize the economy in the long run.

We aren’t out of the inflationary woods yet… But the Fed is taking the right steps toward navigating it.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

To see our best macro insights, become an FA Alpha and get access to FA Alpha Pulse.